Life Insurance in Japan: An Expat's Guide to Coverage and Tax Deductions

Navigate life insurance in Japan as an expat. Understand term vs. whole life, the inheritance tax tax-free exemption, and how to claim the premium tax deduction.

YenWise Editorial

Japan personal-finance research for expats

For expats living in Japan with dependents, securing life insurance is a critical element of financial and estate planning. Beyond the peace of mind it offers, life insurance in Japan comes with unique legal and tax benefits — including specific deductions that reduce your income tax and a dedicated exemption that shields payouts from inheritance tax.

The "Liquidity Bridge" After Death

One of the most important reasons to have a Japanese life insurance policy is immediate liquidity. In Japan, when a person passes away, their bank accounts are immediately frozen by the banks. These accounts cannot be accessed until the entire inheritance process is finalized, which requires consensus among all statutory heirs and can take several months. Life insurance payouts, however, are typically paid out to the designated beneficiary within a few days, providing a crucial financial bridge for surviving family members to cover living expenses, funeral costs, and immediate bills.

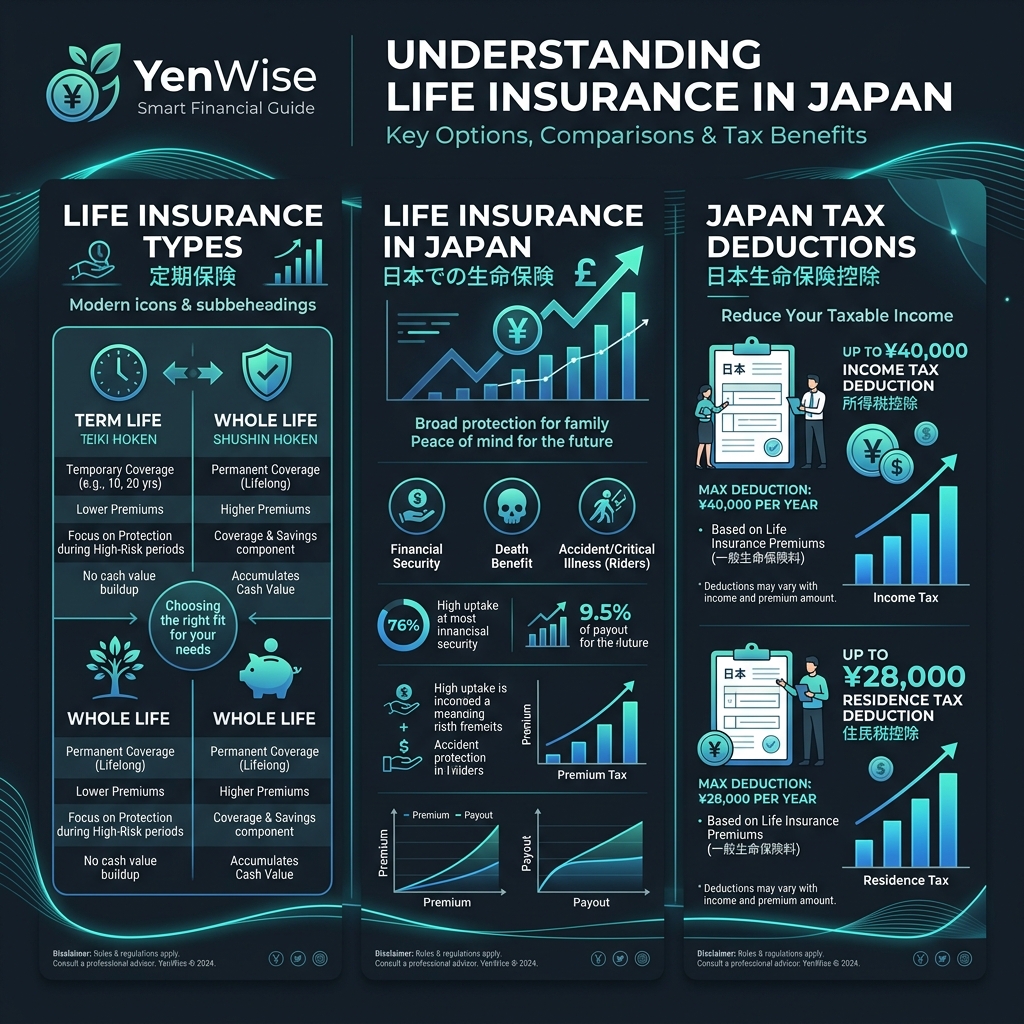

Term Life (Teiki Hoken) vs. Whole Life (Shushin Hoken)

When choosing a policy in Japan, you will primarily decide between two structures:

- Term Life Insurance (定期保険 — Teiki Hoken): Provides coverage for a specific period (e.g., 10, 20 years, or until age 60/65). It is pure protection with no cash value, making premiums highly affordable. This is ideal for families wanting coverage while their children are growing up.

- Whole Life Insurance (終身保険 — Shushin Hoken): Provides lifetime coverage and builds cash value over time. It can function as a savings vehicle, but premiums are significantly higher. Some policies allow you to borrow against the cash value or receive it as an annuity in retirement.

The Inheritance Tax Exemption for Life Insurance

Under Japanese tax law, life insurance payouts are subject to inheritance tax rather than income tax (provided the deceased paid the premiums). However, the government provides a generous tax-free exemption specifically for life insurance payouts:

Tax-Free Exemption = ¥5 million × number of statutory heirs

For example, if you leave behind a spouse and two children (3 statutory heirs), the first ¥15 million of your life insurance payout is completely exempt from Japanese inheritance tax. Any amount above this limit is added to the rest of your estate for progressive inheritance tax calculation.

Maximizing the Life Insurance Premium Tax Deduction

You can deduct a portion of your life insurance premiums from your taxes every year. The Life Insurance Premium Deduction (生命保険料控除 — Seiho Kojo) is divided into three categories: general life insurance, individual annuity insurance, and nursing/medical care insurance.

For policies signed after January 1, 2012, you can deduct up to ¥40,000 from your national income tax and up to ¥28,000 from your local residence tax per category, leading to a maximum combined deduction of ¥120,000 (income tax) and ¥70,000 (residence tax) if you hold policies in all three categories.

For regulatory updates, consult the Financial Services Agency (FSA) and review educational materials provided by the Life Insurance Association of Japan.