Japan Tax Residency: Income Tax vs Inheritance Tax Rules for Expats

Confused about when Japan considers you a tax resident? Here is how the 5-year income tax rule and 10-year inheritance tax rule actually work — and why your visa type matters.

YenWise Editorial

Japan personal-finance research for expats

One of the most confusing aspects of Japan's tax system is that there is no single definition of "tax resident." Instead, different taxes use different rules with different timelines — and your visa type can completely change whether you owe tax on overseas assets and income.

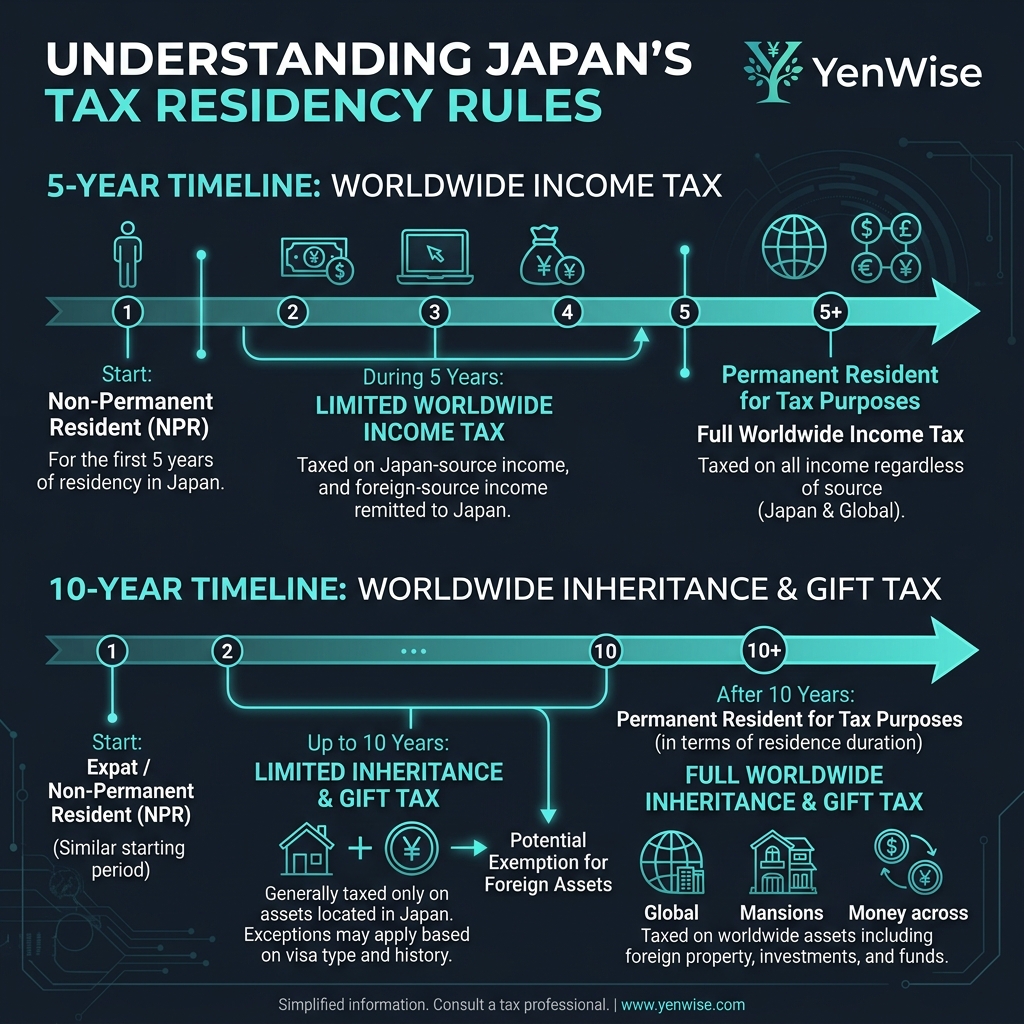

Income Tax Residency: The 5-Year Rule

For income tax purposes, you become a "permanent resident for tax purposes" after living in Japan for 5 years out of the last 10. Once you cross this threshold, Japan taxes your worldwide income — including salary from overseas employers, foreign rental income, dividends from foreign stocks, and capital gains on foreign assets.

The ¥50 Million Foreign Asset Reporting Rule

Permanent tax residents with foreign assets exceeding ¥50 million must file an annual Statement of Foreign Assets (国外財産調書) with the NTA. Failure to file can result in penalties of up to 1 year in prison or a ¥500,000 fine. This reporting requirement catches many long-term expats by surprise.

Inheritance Tax Residency: The 10-Year Rule (And Visa Exceptions)

Inheritance tax uses a completely different residency test. The general rule: if you have lived in Japan for 10 years out of the last 15, you are liable for inheritance tax on worldwide assets — including inheritances received from family members overseas.

The Visa Type Exception That Most Expats Miss

Here is the critical detail: the 10-year rule only applies to holders of Table 1 visas (work visas, student visas, etc.). If you hold a Table 2 visa — which includes spouse visas, permanent residency (PR), and long-term resident visas — you are liable for inheritance tax from day one, regardless of how long you have lived in Japan.

Exit Tax: What Happens When You Leave Japan

If you are a permanent tax resident who holds ¥100 million or more in total assets (domestic + foreign), leaving Japan triggers an exit tax (出国税) on unrealized capital gains. This is a deemed-disposition rule — Japan treats your assets as if you sold them at market value on your departure date, and taxes the gain. For most expats this does not apply, but high-net-worth individuals need to plan ahead.

Practical Steps for Compliance

- Know your visa type. Check if you hold a Table 1 or Table 2 visa — this determines your inheritance tax liability timeline.

- Track your time in Japan. The 5-year income tax clock and 10-year inheritance tax clock run independently.

- File foreign asset reports if required. If you are a permanent tax resident with >¥50M in foreign assets, the Statement of Foreign Assets is mandatory.

- Plan for exit tax if applicable. If your total assets exceed ¥100M, consult a tax professional before leaving Japan.

For official details, see the NTA's guide on tax residency and the Ministry of Justice visa table classifications.