iDeCo Explained: Japan's Secret Tax Break That Saves Expats ¥300,000+ Per Year

iDeCo (Japan's individual-type defined contribution pension) offers immediate tax deductions and tax-free growth. Here's how much you can save and who qualifies.

YenWise Editorial

Japan personal-finance research for expats

While everyone talks about NISA, iDeCo (個人型確定拠出年金 — Individual-type Defined Contribution Pension) is arguably Japan's most powerful tax-saving tool for expats planning to stay long-term. Under this program, the government essentially subsidizes your retirement savings by letting you invest pre-tax income.

How iDeCo Saves You Money: Triple Tax Advantage

- Tax-Deductible Contributions: Every yen you contribute reduces your taxable income. At a 33% marginal rate, a ¥23,000/month contribution saves you ¥7,590/month in taxes.

- Tax-Free Growth: All gains inside iDeCo grow tax-free — no 20.315% capital gains tax.

- Tax-Free Withdrawal: At retirement (age 60+), withdrawals receive special retirement income treatment with large tax-free allowances.

How Much Can You Contribute?

Your monthly contribution limit depends on your employment category:

- Self-employed (Category 1): Up to ¥68,000/month — the highest limit

- Company employee, no corporate DC plan (Category 2): Up to ¥23,000/month

- Company employee, with corporate DC plan (Category 2 DC): Up to ¥12,000/month

- Full-time homemaker / dependent spouse (Category 3): Up to ¥23,000/month

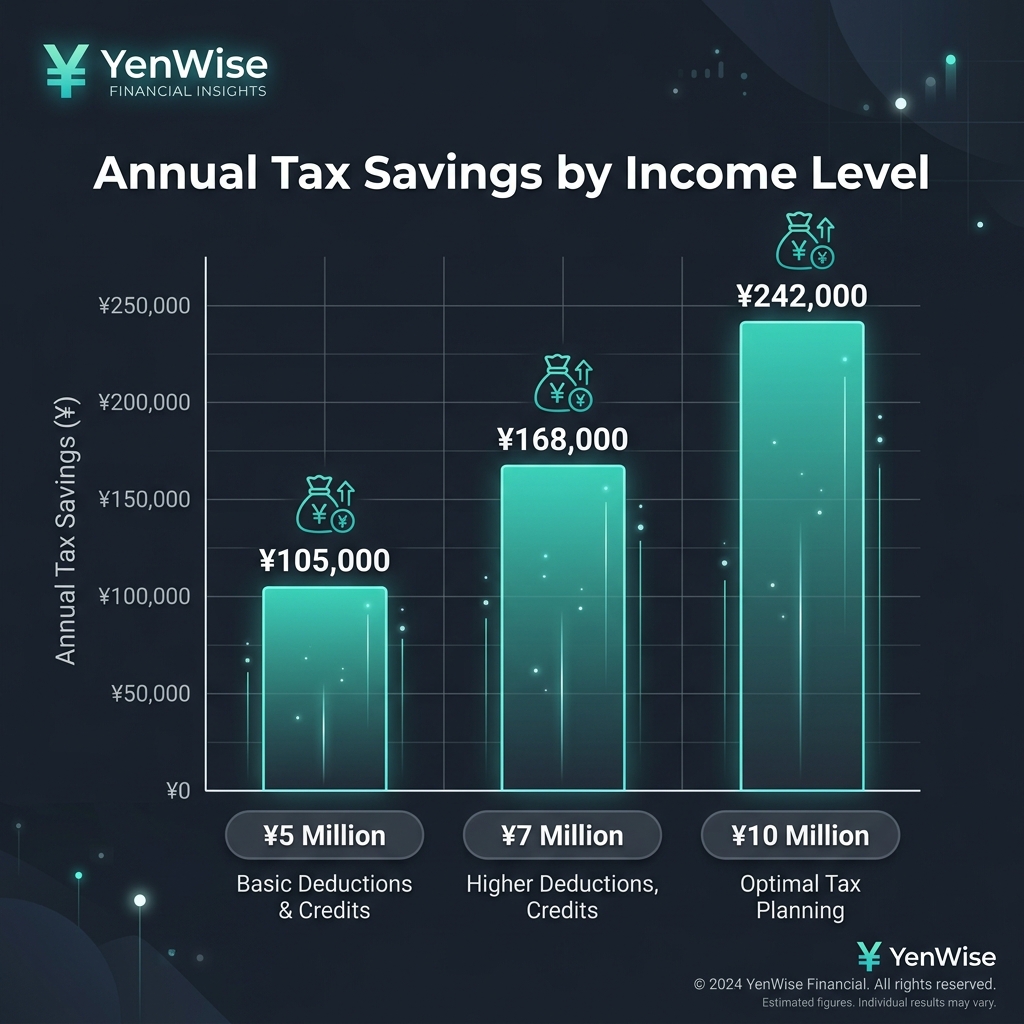

The Tax Savings: Real Numbers

Let's look at a concrete example. A 35-year-old company employee earning ¥7M/year with no dependents would have the following iDeCo projection:

- Monthly contribution: ¥23,000 (Category 2 max)

- Annual contribution: ¥276,000

- Marginal tax rate: 20% income tax × 1.021 surtax + 10% residence tax = 30.42%

- Annual tax savings: ¥276,000 × 30.42% = ¥83,959

Over 25 years (age 35→60), that's ¥2,099,000 in pure tax savings — PLUS tax-free investment growth. Run your own numbers with our iDeCo calculator.

The Locked-Until-60 Rule

The biggest catch with iDeCo: your money is locked until age 60. You cannot withdraw early, even in an emergency. If you leave Japan permanently before age 60, you face a difficult choice:

- Leave it invested until age 60 — funds continue growing tax-free. You'll need a Japanese bank account.

- Early lump-sum withdrawal — possible if you've contributed for less than 5 years and meet specific criteria. Taxed as ordinary income.

iDeCo vs NISA: Quick Comparison

- iDeCo: Immediate tax deduction, locked until 60, great for retirement, calculate savings →

- NISA: No upfront deduction, withdraw anytime, great for flexibility, calculate returns →

- Both?: Many expats max iDeCo for retirement + NISA for medium-term goals

How to read the tax savings without over-trusting them

iDeCo’s headline benefit is the income-tax and residence-tax deduction on contributions. The exact yen saved depends on your marginal brackets, other deductions (including furusato nozei and insurance), and whether you are a salaried employee in year-end adjustment or file a final return. Our iDeCo calculator shows a transparent estimate; treat it as a planning range, then confirm with your payslip or a zeirishi if the amount is material to a decision.

Contribution limits and category mistakes

Limits differ for company employees with/without a corporate DC plan, public servants, self-employed Category 1 insured, and other statuses. Entering the wrong category is the most common user error. If you changed jobs mid-year, your effective monthly ceiling can change — re-check the National Pension Fund Association tables and re-run the calculator after the switch.

- Confirm your pension category before maxing contributions

- Coordinate iDeCo with NISA: deduction vs liquidity

- Model early departure from Japan — lock-up until 60 is real

- Keep contribution records for year-end adjustment or 確定申告